How to save Money on Capital Gains Tax

How do you save money on Capital Gains Tax? For an Accountant this is a question which is asked regularly. But as you can always find a way to save money. Below I give you a basic insight into how CGT (Capital Gains Tax) works, some tips, exceptions and how to avoid it completely:

How does it work? CGT is run through the tax year (6th April one year to 5th of April the following year). It is worked out on the total of your taxable profit from any capital assets that you hold. For instance, property, bonds and shares on the stock exchange. Furthermore, it is when the amount exceeds the purchase price of a property, bond and shares/stock. The amount that is exempt (tax free) annually is £10,900 for 2013 to 2014 (which increases to £11,000 for 2014 to 2015). At present there are two different types of CGT. The basic rate taxpayers pay is 18%, although the higher rate tax payers pay is 28% and if the capital gains goes over your threshold you will pay the higher tax. Tips to save money Below are some tips to keep the CGT Low as possible:

Exceptions Any profit made on selling your home is tax exempt, unless you did one of the options below:

You can also get away with not paying tax if you make a profit on selling a car, ISA’s, Peps, UK government gifts, savings certificate, premium bonds, personal belongings that are worth £6,000 or less when you come around to selling them. Furthermore there is a 10% tax rate with the entrepreneur’s allowance, which is aimed to help people that are selling their businesses they have built up. It has a lifetime limit of £5m. Avoid it completely If you want to avoid paying the higher threshold of 28% there are some suggestions below:

You can defer your CGT by reinvesting it into the Enterprise Investment Scheme (EIS). You would have a limit of £200,000. Furthermore, any profit made will be exempt if you meet the qualifying standards. Finally, while tax avoidance is legal, tax evasion is illegal. So do not be tempted to sell assets without declaring any profit to HMRC. Defrauding the tax man can land you with a large fine or even a prison sentence. But the advice and support of an experienced tax accountant and some sound forward tax planning can save you thousands of pounds. By Tahir Malik at Tax Affinity Accountants Tax Affinity Accountants are experts in Tax and Accountancy. Based in Kingston upon Thames they are considered in the Finance Industry to be the experts in all types of Tax including Capital Gains Tax. Helping and supporting businesses and individuals throughout the UK, they regularly help people with their CGT tax issues. For more information visit www.taxaffinity.com. To read more interesting articles like this visit www.taxaffinity.com/blog. Please feel free to comment and share this with your friends.

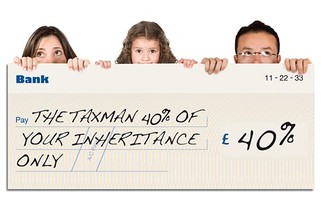

Plan Plan Plan ahead to save Inheritance Tax

Saving Inheritance tax

Inheritance tax can be a tricky issue to deal with for most people but it is generally considered a “voluntary tax” as good tax planning can greatly reduce your inheritance tax liability or erase it completely. Assets exceeding the current inheritance tax threshold of £325,000 (for tax year 13/14) are taxed at 40%. That’s basically half of your excess assets going straight to the government and not to your loved ones. This is why inheritance tax can be extremely costly for those who have not done sufficient planning. Fortunately, there are many exemptions and allowances to utilise which would significantly reduce the amount of inheritance tax you have to pay. Here are a few things to consider that can help you save some inheritance tax:- Make a Will Making a will allows you to know that your estate is divided exactly as you want it to be when you die. In the absence of a will, people that you wish to benefit from your estate such as an unmarried partner may not be entitled to any share in the event of intestacy. What is a gift? A gift is something of value given unconditionally to someone without any reservations. The biggest asset that most people are in possession of is their house. However, giving away your house yet trying to live in it may allow HMRC to invalidate the gift as genuine and apply tax on it. Give away sooner Majority of gifts you make are classified as “potentially exempt transfers”. If you survive more than seven years after making the gift, no inheritance tax is due on that gift. The amount of tax can be reduced depending on how long you lived after making the gift due to taper relief. Gifts made less than three years before death have no reduction in tax. If the gift was made three to four years before death then tax is reduced by 20%. This increases by 20% for every extra year the donor lives up to seven years where the whole amount is exempt. Therefore it can help relief some financial burden on your death estate if you make gifts sooner rather than later. Allowances to take advantage of You can give away gifts worth up to £3,000 in total per person every tax year and these gifts will be exempt from inheritance tax when you pass away. Any unused part of this annual allowance can be carried forward to the following year, but if you don’t use it in that year, the carried-over exemption expires. You can also give up to £5,000 to your children when they marry as a wedding gift. Grandparents can give up to £2,500 and others up to £1,000. Regular Gifting Regular gifting can dramatically reduce your inheritance tax bill as long as they meet the following criteria: they must be from your income, they must be regular and they must not decrease the standard of living of the donor. Be generous on birthdays Gifts under £250 to any recipient per tax year are exempt from inheritance tax. This means that it might be worth giving your boy a big birthday present even if he’s been naughty as it helps reduce the tax bill. Gifts to charities and political parties are tax-free It’s good to know that any donations you make to charities or political parties are inheritance tax free at least. Getting Tax Advice While it is generally more economical for you to do things by yourself, if you have sizeable assets then seeking professional tax advice is well worth your money. You may end up paying a few hundred pounds to potentially save over hundreds of thousands of pounds. I’m no bargain hunter but that sounds like a good deal to me. By Wilson Law at Tax Affinity Accountants Tax Affinity Accountants are experts in Tax and Accountancy. Based in Kingston upon Thames they are considered in the Finance Industry to be the experts in all types of Tax including Inhertance Tax. Helping and supporting business and individual throughout the UK, they regularly help people with their Inhertance tax issues. For more information visit www.taxaffinity.com. To read more interesting articles like this visit www.taxaffinity.com/blog. Please feel free to comment and share this with your friends.

Its always there in the back of your mind...

Personal Tax Return Deadline Approaches

Completing a personal tax return can be a stressful, complex task and an unwanted hassle for self assessment taxpayers. At Tax Affinity we provide a simple, price competitive service to alleviate your concerns over personal tax returns. If you currently complete your own tax return then you could certainly benefit from our services to ensure that you don’t overpay on tax. Mistakes on your tax return could cost you a significant amount and it is therefore worth taking advantage of expert advice to make sure you report the correct level of taxable income. We will assess all of your income and expenses information to ensure you minimise your tax liability. If you are already taking advantage of our tax help, please ensure you send us all your income and expenses information (bank statements, invoices and receipts) for the period 6th April 2012- 5th April 2013 as soon as possible. With the busy Christmas and New Year period approaching, it is vital that we receive all this information in the next 3-4 weeks so we can ensure all of our clients’ tax returns are submitted before the deadline. By leaving your tax return right up until the last minute you risk incurring a late filing penalty. Here is a summary of the HMRC penalty charges you may face: Length of Delay - Penalty incurred 1 day late A penalty charge of £100 even if you have no tax liability for the year or have paid the tax you owe 3 months late A penalty charge of £10 per day up to a maximum of 90 days- £900. This is on top of the initial £100 charge. 6 months late £300 or 5% of the tax due (whichever is higher). On top of the penalties listed above 12 months late An additional £300 or 5% of tax due. However, in certain cases the charge may be up to 100% of the tax due or higher. Please avoid any of these penalties by sending us all your information as soon as possible. Feel free to pop into the office or just email us the necessary documents. Rushing a tax return can result in a number of unnecessary errors so please ensure you get on top of the situation in the coming weeks. By Tom Hoadley at Tax Affinity. Tax Affinity Accountants are experts in Tax and Accountancy. Based in Kingston upon Thames they regularly submit tax returns for their clients peace of mind, providing a great value for money service for people from all walks of life. For more information visit www.taxaffinity.com. To read more interesting articles like this visit www.taxaffinity.com/blog. Please feel free to comment and share this with your friends.

Every year many people across the UK get a tax credits renewal pack. If you do get one you need to check your renewal forms and make sure you pass on the correct information to the Tax Credits Dept.

This article can help you find out some of the information you need to check, how to work out your personal income(s), and how to avoid common mistakes. Check the information presented Renewal packs usually include the an Annual Review notice (TC603R) plus an Annual Declaration form (TC603D or TC603D2). And everyone needs to renew by 31 July or whatever date is shown on letters from HMRC. A tax year runs from 6 April one year to 5 April the next. The important information that you need to check on your Annual Review notice is:

If there is anything incorrect you must tell HMRC straight away. Especially if anything is wrong on your notice or if anything has changed and they have the wrong information. If previously you have claimed tax credits as a single person - or as a couple your notice should say this, a couple is known as a 'joint' claim. You should be making a 'joint' claim if you are:

Your form should also show the country you live in most of the time. It doesn't matter if you sometimes go to other countries for holidays for up to 8 weeks (and in some cases up to 12 weeks) as this is usually still allowed. And you may also be able to get tax credits if you live outside of the UK for a valid reason. But you will need to confirm these extra conditions with HMRC before applying for them. Your work or benefits should also be reported, showing the country you work in most of the time with the number of hours a week you usually work. It can also show you if you got any benefits, for example Income Support or Employment and Support Allowance. If you have any disabilities your notice will explain if you were paid the disability part of Working Tax Credit. This also applies to severe disabilities and their allowances receivable. If you have a child or children then your notice should show the correct information about them. You can usually get Child Tax Credit for a child up to 20 years old, with the conditon that they are in full-time education or an approved training course. And if you work are working at least 16 hrs per normal week and have to pay for a registered or approved child minder or carer, you may be able to get an extra Working Tax Credit payments to help with these costs too. How to work out your total income for your Annual Declaration It is worth noting that some social security benefits are taxable, such as contribution-based JSA (Job Seeker's Allowance), and as such they will count as income when you make a tax credits claim. Other types such as Disability Living Allowance, don't count as income. So be careful to be sure if your benefit is taxable. If your not sure ask rather than guessing and getting the claim incorrect. If you're in employment, you should have a P60 from your employer at the end of the tax year (5th April), which will show your earnings and tax paid for the whole tax period (6th April to 5th April). You need to include income from all types of jobs you have had in the tax year so it may need several P60's for filling it in. If you cannot find your P60, then don't worry as most payslips usually show a running total of all earnings and tax paid for the year. If you still cannot get the full information you can provide an estimate but make sure to give the actual income figure no later than 31 January or again it can mean having to pay tax credits back at a later date if you've claimed to much. You must also remember to add in:

If you're self-employed your income will be the net profit you made in the tax year. If you haven't had a profit or loss drawn up prior to sending in your tax return, then you will need to give an estimate of your profit and again you must provide an actual by the 31st January or you may have received too much or less in Tax Credits. If you made a Net Loss on self employment, just give a figure of zero. But please do note if you had any other income during the year, you can take the loss off this income. Be careful to get the best advice and support Bear in mind that other income like pensions, shares, income from property (sale or rental), income that you receive from abroad and savings need to be also declared. If in doubt the best thing to do is ask a professional as the self employment and other incomes can become a bit tricky and you could end up claiming less or more than your due. Tax Affinity Accountants are experts is tax and accountancy. Based in Kingston upon Thames they cover the whole of the UK and help make sure clients get the correct amount of tax credits for their situations. Visit www.taxaffinity.com for more information or if you feel you need help in filling in the forms. Follow Tax Affinity on twitter at @tax_affinity to find other useful tips and advice.

Small firms get more time to get ready for RTI submissions

HMRC has announced that it will be extending the new Real Time Information (RTI) reporting rules for businesses with fewer than 50 employees from October 2013 until April 2014. This new extension now means that businesses are not required to change their approach halfway through this tax year. But small businesses are still required to report through the new system on a monthly basis, rather than each time they pay their employees. This allows many businesses that pay weekly (or more) to report monthly instead of everytime they pay a member of staff. HMRC, says that more than 1.4 million employer PAYE schemes are now reporting in real time since the start of the new tax reporting requirements in April. According to HMRC 83% of SMEs and more than one million micro employers have already started to report PAYE in real time. HMRC goes on to say that from April 2014, all employers in the UK will need to plan to be reporting in real time, but also say it is continuing to work with businesses over the coming months to identify whether there are any specific circumstances that it needs to cater for the long term. HMRC's director general for personal tax, said: "The roll-out continues to exceed our expectations. We will now write to the minority of employers who are not on board, to establish how we can help them meet the requirements of reporting in real time." This extension for small businesses with less than 50 staff, till April 2014 is very helpful for SME's. It will help them continue to engage positively with RTI and to keep the costs of RTI reporting as low as possible. At Tax Affinity Accountants we are experts in Payroll and are already helping our clients submit their payroll information on time and regularly to HMRC, feel free to contact us if you need help in your RTI complaince at www.taxaffinity.com. In the current economic climate everyone should be looking for ways to save tax. And to help, we at Tax Affinity Accountants have compiled a list to do just that.

The tax codes, allowances and deadlines 1. Tax code Check your tax code each year (the numbers and letters on your payslip). If you're on the wrong code, you may be paying too much tax. 2. Capital gains tax allowance Remember that capital gains under £10,600 are tax-free. Married couples and civil partners who own assets jointly can claim a double allowance of £21,200. CGT is charged at 18% if you are a standard rate taxpayer, and 28% if you pay tax at a higher rate. 3. Tax return deadlines Don’t miss the 31 October deadline if you want to make a paper tax return. You can do your tax online up to 31 January, but paper tax returns need to be in three months earlier than online tax returns to avoid a £100 fine. 4. Annual investment allowance If you are a landlord or run your own business, take advantage of the annual investment allowance (AIA) to claim for capital expenditure on items such as tools and computers. You can claim relief on up to £25,000 a year. How to pay less tax if you're self-employed 5. Tax-deductible expenses If you’re self-employed, don’t forget to claim all your tax-deductible expenses, including cash expenditure where eligible. 6. Self-employed car costs If you're self employed, you can claim the running costs of a car, but not the cost of buying one. If you use the same car privately, you can claim a proportion of the total costs. 7. Cash-flow boost for self-employed If you are setting up as self employed, you may be able to improve your cashflow by choosing an accounting year that ends early in the tax year. This maximises the delay between earning your profits and your final tax demand. 8. Annual losses If you are self employed, you can carry forward losses from one year and offset them against profits from the next. See our page on when the self-employed pay tax for more. 9. Payments on account If you are self-employed and expect to earn less in 2012-13 than you did the year before, apply to reduce any payments on account that HMRC ask you to make. Saving tax on property income 10. Rent a room Rent a room relief is an optional scheme that lets you receive up to £4,250 in rent each year from a lodger, tax-free. This only applies if you rent out furnished accommodation in your own home. 11. Landlord's energy-saving allowance If you rent out property you can claim special tax allowance of up to £1,500 for insulation, draught proofing and installing a hot water system. 12. Landlord's expenses If you rent out property, you can deduct a range of costs before declaring your taxable income. These include the wages of gardeners and cleaners, and letting agency fees. 13. Tax relief on your mortgage You can claim tax relief on the interest on a mortgage you take out to buy a rental property – even if it the rental property is abroad. 14. Reduce capital gains tax (CGT) on a rental property Landlords are normally liable for CGT when they sell a rental property. If it has been your main home at some time in the past, you can claim tax relief for the last three years of ownership. Pay less tax on savings and investments 15. Isa allowance Use your tax-free Isa allowance. This year, the overall limit is £10,680, of which £5,340 can be put into in a cash Isa. 16. No CGT on shares held in an Isa There is no capital gains tax to pay when you sell shares or units held in an Isa. For more details see Tax on savings and investments. 17. Junior Isas Use Junior Isas or Children’s Bonus Bonds to avoid being taxed on gifts you make to your own children. 18. Transfer assets Transfer savings and investments to your husband, wife or civil partner if they pay a lower rate of tax than you do. See our guide to tax and your partner for more information. 19. Children's savings Stop children being taxed at source on their savings by completing a simple form (R85) on their behalf. Tax savings for older people 20. Age-related allowance If you are aged 65-plus you may be eligible for an increased personal allowance. This means you pay a lower income tax rate. See Tax in retirement. 21. National Insurance Make sure you stop making National Insurance contributions if you carry on working beyond state retirement age (currently 62 for women and 65 for men). 22. Gift Aid If you are over 65, making donations to charity through Gift Aid can reduce your taxable income to below the threshold at which you start to lose out on age-related allowances. 23. Tax relief on gifts If you are in a higher tax bracket, you can claim back the difference between the basic and higher rate of income tax on any Gift Aid donations. 24. Inheritance tax Lifetime gifts are not normally counted as part of your estate for inheritance tax purposes if you live for a further seven years after making them. Known as potentially exempt transfers (PETs) they can reduce your residual estate significantly. See our blog on inheritance tax. Tax savings through employee benefits 25. Season ticket loan If you are a commuter, check to see if your employer will give you a tax-free loan to buy your season ticket. 26. Pool cars Use a pool car for occasional business travel, if your employer provides these. 27. Childcare schemes and tax credits If you are an employee and pay for childcare, ask your employer if they have a childcare scheme. Salary sacrifice childcare schemes are easy to establish and can result in substantial savings for both employees and employers. For more details see working for an employer. Child tax credits can also save you money. 28. Company car? If you are entitled to a company car, consider whether it would be more tax-efficient to take a cash equivalent in pay instead. 29. Going green If you are changing your company car, consider a low-emissions model . These are now taxed at a lower percentage of their list price, than cars with a high CO2 rating. 30. Pay in to a pension scheme Contributions to your employer's pension scheme (including any additional voluntary contributions you make) can be made from your gross pay, before any tax is charged. For the most up to date and accurate advice speak to tax accountant, as these allowances and benefits do change every year. Tax Affinity Accountants are expert Qualified Tax Accountants in Kingston upon Thames. To read more visit www.taxaffinity.com/blog and please feel free to comment and share this with your friends. |

Various AuthorsOur experienced accountants and tax advisers provide valuable insights into practical every day questions and issues. Archives

March 2024

Categories

All

Ask your own question: If you would like to have a tax related question answered here, please send your question to info@taxaffinity.co.uk. |

RSS Feed

RSS Feed